Leverage products

Warrant with Knock-Out

Leveraged products are financial instruments that enable traders to gain greater exposure to the market without increasing their capital investment. They do so by using leverage.

Any financial instrument that allows you to take a position that is worth more on the market than your initial outlay is a leveraged product. Different leveraged products work in different ways, but all amplify the potential profit and loss for a trader.

Leveraged products will almost always require you to pay an initial portion of the position you intend to open. This is called the margin.

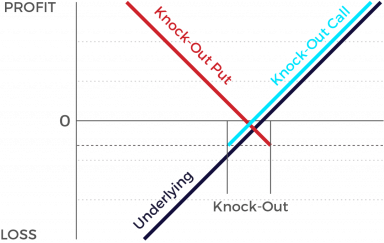

Market expectation

- Knock-Out (Call): Rising underlying

- Knock-Out (Put): Falling underlying

Characteristics

- Small investment generating a leveraged performance relative to the underlying

- Increased risk of total loss (limited to initial investment)

- Suitable for speculation or hedging

- Continuous monitoring required

- Immediately expires worthless in case the barrier is breached during product lifetime

- Minor influence of volatility and marginal loss of time-value

Graphic

Knock-out Warrants: Knock-out warrants are also leverage investment products but have several characteristics that differ from those of call or put warrants: - Knock-out warrants can expire prematurely if the price of the underlying instrument falls below (in the case of knock-out calls) or exceeds (in the case of knock-out puts) a predetermined level. Depending on the features of the given product, it then expires worthless or a specified amount is paid back to the investor. - Changes in implied volatility have little or no impact on knock-out products, therefore their pricing is easier for investors to comprehend than in the case of warrants. Knock-out products possess little or no time value and have a higher degree of leverage than similarly structured warrants. - Due to the possibility of getting “knocked out”, as well as the higher degree of leverage involved, knock-out products are riskier than other types of warrant. Premium: As is the case with normal warrants, issuers of knock-out warrants establish hedges by buying or selling the underlying instrument so they don’t have to speculate against investors. However, due to the leverage of knock-out calls, the issuer who sells them to the public has to invest a significantly greater amount of capital than the investors do. Thus the issuer essentially passes-through to investors the related interest costs by means of the premium. When they sell knock-out puts to investors, issuers must short the underlying instrument in order to establish a hedge. As a result, they receive capital that can be invested to earn short-term interest. For that reason, it’s not rare that that knock-out puts actually trade with a negative premium (discount), in which case the product costs less than its intrinsic value. Leverage: The leverage of knock-out warrants can be calculated as follows: (price of underlying instrument x exercise ratio) / price of knock-out warrant = (CHF 55.00 x 0.1) / CHF 0.57 = CHF 9.65 Consequently, the knock-out call in our example would gain almost 10% in value if the price of Holcim stock rises by 1%. But bear in mind that all valuation factors are a snapshot at a moment in time and, as we said before, leverage is a door that swings both ways. Price declines in the underlying instrument can rapidly lead to very large losses. And if Holcim stock trades at or below the CHF 50.00 mark, you’ll incur a total loss unless you’ve sold your holdings prior to the knock-out event. The greater the leverage of a knock-out product, the greater the opportunity to profit from it. But the risk is also greater. When buying knock-outs, investors should absolutely make sure that there is a sufficient buffer between the price of the underlying instrument and the knock-out level. Product types: Generally speaking, there are two different types of knock-out products: - Knock-out warrants without a stop-loss level: For this type of product – as is the case in our previous example – the strike price and knock-out threshold are identical. - Knock-out products with a stop-loss level: For this type of product, the knock-out threshold lies above (calls) or below (puts) the strike price. If the knock-out level is violated, the product also terminates immediately but as a rule you will receive payment of a residual value. Because the knock-out level for these products acts like a normal stop order, that threshold is usually referred to as the “stop-loss level”. At the time they are issued, most knock-out products have a term to expiration of several weeks to several months. But some knock-outs feature an unlimited term and termination only once the price of the underlying security touches or penetrates the stop-loss level. These products have no premium, thus their price always corresponds to their intrinsic value. Because the interest associated with the issuer’s hedging operations also applies to open-end products, the exercise price (financing level) and stop-loss level are adjusted at regular intervals, thus the intrinsic value of the products also changes. So it’s important to know that, in the case of a longer holding period, the intrinsic value of such a knock-out warrant can decline if the price of the underlying instrument simply trades sideways.